In that sense, we will see a smaller ending inventory during inflation compared to a non-inflationary period. This article will cover how to determine ending inventory by LIFO after selling in contrast to the FIFO method, which you can discover in Omni’s FIFO calculator. Also, we will see how to calculate its cost of goods sold using LIFO, and show how to use our LIFO calculator online to make more profits. Perpetual inventory methods are increasingly being used in warehouses and the retail industry.

- Under last-in, first-out (LIFO) method, the costs are charged against revenues in reverse chronological order i.e., the last costs incurred are first costs expensed.

- For the past 52 years, Harold Averkamp (CPA, MBA) hasworked as an accounting supervisor, manager, consultant, university instructor, and innovator in teaching accounting online.

- The nature and type of business you have will factor into the kind of inventory you use.

- Petersen and Knapp allegedly participated in channel stuffing, which is the process of recognizing and recording revenue in a current period that actually will be legally earned in one or more future fiscal periods.

- Even though GAAP standards say that either perpetual or periodic systems are appropriate for any business, each is more suited to different-sized organisations.

Mục lục

What Is FIFO?

So let’s go ahead and pause here and then we will start an example of how to use these methods in a perpetual system. Perpetual inventory and periodic inventory are both accounting methods used by businesses to track the number of products they have available. The two systems also differ in how they calculate Cost of Goods Sold (COGS). In a perpetual inventory system, COGS is calculated automatically after each sale by multiplying the number of units sold by their respective costs per unit (source). Conversely, in a periodic inventory system, COGS is determined manually at specific intervals using beginning and ending inventories along with purchases made during that period.

A Summarized Guide to Inventory Costing Methodologies

For the past 52 years, Harold Averkamp (CPA, MBA) has worked as an accounting supervisor, manager, consultant, university instructor, and innovator in teaching accounting online. This is slightly different from the amount calculated on the perpetual basis which worked out to be $2300. Therefore, the value of ending inventory under both systems will usually differ when applying the LIFO basis. Let’s see the LIFO method in action in a more complete example below that includes a range of transactions.

Does a perpetual inventory system use FIFO or LIFO?

Therefore, your company has a lower tax liability in a LIFO system, because businesses get taxed on profit. The Internal Revenue Service allows companies to use LIFO in their tax accounting, even when they use FIFO in their financial statements. In a perpetual system, you will sometimes need to estimate the amount of ending inventory for a period when preparing financial statements or if stock was destroyed. To calculate this estimate, start with the beginning inventory and cost of purchases during the period. A perpetual inventory system is a program that continuously estimates your inventory based on your electronic records, not a physical inventory. This system starts with the baseline from a physical count and updates based on purchases made in and shipments made out.

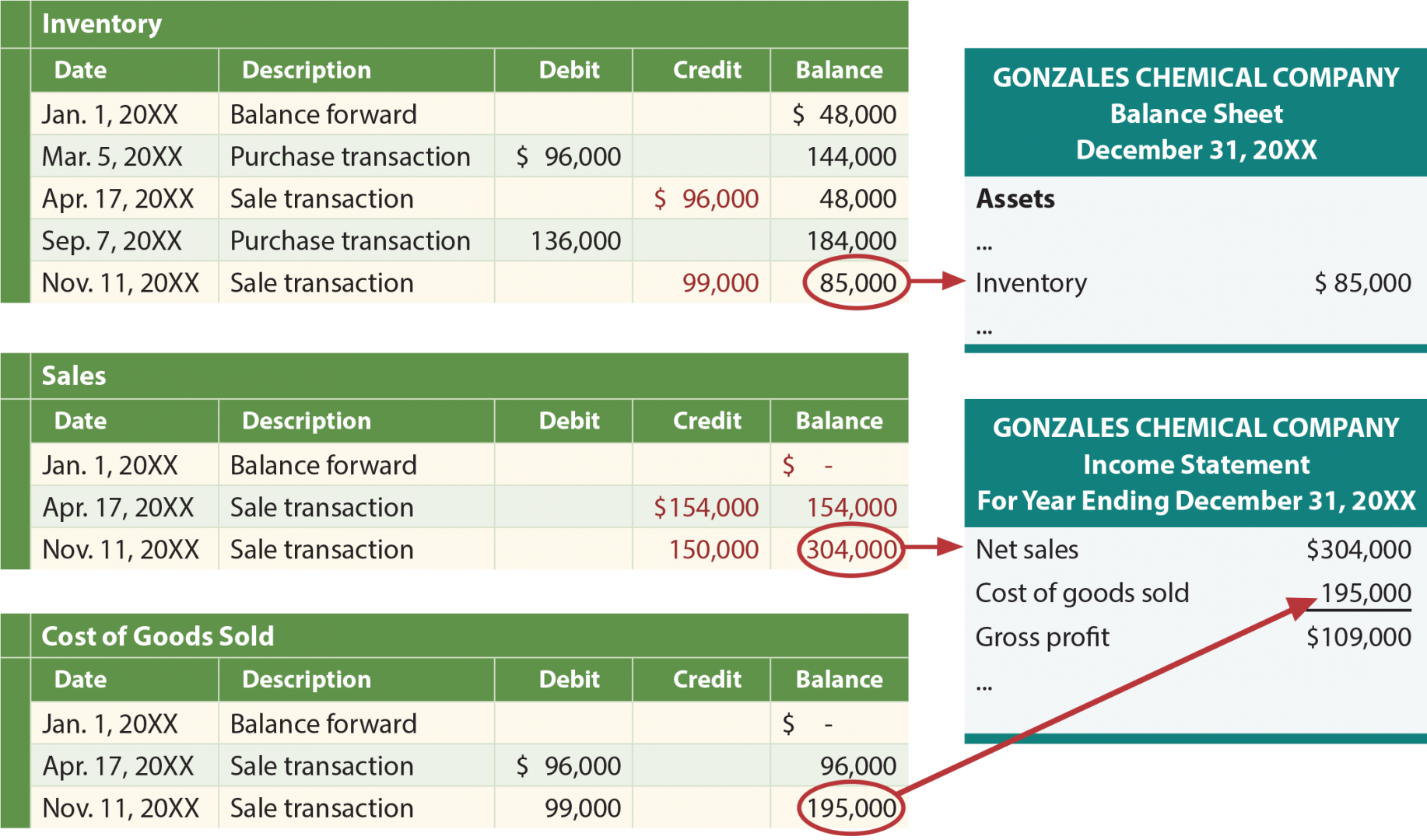

(Under the periodic system, the account Purchases was debited.) When the retailer sells the merchandise, the Inventory account is credited and the Cost of Goods Sold account is debited for the cost of the goods sold. Rather than the Inventory account staying dormant as it did with the periodic system, the Inventory account balance is updated for every purchase and sale. According to a physical count, 1,300 units were found in inventory on December 31, 2016. The company uses a periodic inventory system to account for sales and purchases of inventory. The goal of using the WAC is to give every inventory item a standard average price when you make a sale or purchase.

Perpetual Inventory System vs. Periodic Inventory System: What’s the Difference?

The only difference between the two cost flow concepts is how rapidly a cost layer is stripped away or replenished in the costing database. Under perpetual LIFO, there can be a great deal of this activity throughout a reporting period, with inventory layers being added and eliminated potentially as frequently as every day. This means that the costs at which items are sold could vary throughout the period, since costs are being drawn from the most recent of a constantly varying set of cost layers. Each time new inventory is purchased, the total cost and quantity are updated, and a new average cost per unit is calculated. After Corner Bookstore makes its third purchase of the year 2023, the average cost per unit will change to $88.125 ([$262.50 + $90] ÷ 4).

In our last transaction above, we withdraw inventory costs from three different layers. The remaining layer from January 5 is only 30 units so we get all of the 30 units and proceed to the last LIFO layer for the remaining 20 units. Under the last-in, first-out assumption, we always remove goods sold from the most recent purchase. This means that the goods sitting in the ending inventory are the earliest purchases. By looking at the purchases schedule in Step 2, we can assign costs to the 80 units by applying the oldest purchase price first.

A perpetual inventory system can utilize the FIFO (First-In, First-Out) or LIFO (Last-In, First-Out) method. The selection of FIFO or LIFO will depend on the particular needs and desires of the company. FIFO is more commonly used as it reflects a natural flow of goods in most industries where older items are sold before newer ones. Let’s explore the LIFO method and discover if this is the best fit for your inventory needs.

So, Lee decides to use the LIFO method, which means he will use the price it cost him to buy lamps in December. To calculate the Cost of Goods Sold (COGS) using the LIFO method, determine the cost of your most recent inventory. Considering that deflation is the item’s price decrease through time, you will see a smaller COGS with the LIFO method. Also, you will see a more significant remaining inventory value because the most expensive items were bought and kept at the very beginning. Please note how increasing/decreasing inventory prices through time can affect the inventory value. Let’s say Ava, a product manager, wants to know if she is pricing generic Acetaminophen high enough to leave a healthy profit margin.

Perpetual and periodic systems require different tools and procedures around how employees document inventory, although they can be complementary. In a periodic system, employees record products only at specified intervals. Ultimately, businesses should carefully assess their specific needs and challenges to determine whether a perpetual inventory system is the right choice.

Economic Order Quantity (EOQ) considers how much it costs to store the goods alongside the actual cost of the goods. The results dictate the optimal amount of inventory to buy or make to minimise expenses. This system depends on proper inventory control procedures.For example, the system needs to ensure that employees scan in any new inventory promptly. Physical counts adjusting entries always include to reconcile the database are rare, but necessary, since the true inventory count can become skewed over time with theft, loss or breakage. Below are some of the most frequently asked questions about using a perpetual inventory system. This section will discuss some of the most common situations where implementing a perpetual inventory system can be highly beneficial.